The Revolution Will Not Be Centralized

The Revolution Will Not Be Centralized

BlockFi's bankruptcy proves that 'crypto banks' were structurally flawed from the outset. FTX's collapse has accelerated the inevitable outcome, and the crypto ecosystem will be stronger as a result.

I haven’t written anything about the ongoing FTX debacle until now, since it’s been covered exhaustively by every news outlet on the planet and there hasn’t been much for me to add to the conversation. I didn’t expect the legend of Sam Bankman-Fried (popularly known as ‘SBF’) to implode as rapidly or as dramatically as it did. That being said, I certainly wasn’t surprised to see it happen.

I never traded on FTX, mostly because I never understood the tokenomics of the FTT token. The relationship with Alameda Research (SBF’s hedge fund) also seemed a bit…murky. (For the record, I feel the same way about Binance’s BNB token today, though at least it’s easier to understand how value accrues to it). Crypto exchanges don’t need a governance token to succeed. Give the people what they want – low fees and lots of liquidity – and they will beat down your front door.

FTX failed because their stakeholders - their customers, as well as some of the most successful investors in the world - gave them a pass. The company had no board, and it was run by a group of kids living in a $40 million Bahamas penthouse who apparently enjoyed exploring ‘Chinese harem’ polyamory together. Yet Sequoia Capital gave them over $214 million, while demanding no oversight, and allowed SBF to invest $200 million of his own capital (actually his customers’ deposits, as it turns out) into their funds.

It’s a shame, really. SBF is a brilliant trader who made enormous amounts of money in 2018 by arbitraging the Bitcoin price between US and Asian crypto exchanges. FTX’s trading engine was world-class, too, and it was a very successful business for its first couple of years. But the founders became greedy and decided to run leveraged trades on customer deposits - a road that normally leads to prison. We’ll see what happens with SBF, who shrewdly became one of the Democratic Party’s biggest donors in recent years and may have accumulated enough political favors to avoid jail, if not career-ending disgrace.

FTX’s collapse has created a ripple effect through the entire crypto ecosystem, since many hedge funds and crypto startups had deposited funds there to trade or generate yield. At least three major funds have failed as a direct result, and I know of at least two venture-backed companies that had stored a majority of their assets on the exchange and will likely need to close down.

More failures may be coming, and it’s certainly not pleasant for those who are impacted, but it’s a natural and highly necessary process. Bear markets are meant to wipe out the excesses and flawed businesses that are built in bull markets. The crypto industry, and particularly all remaining crypto exchanges, will become stronger and more resilient as a result. Auditors will be more demanding, and their investors will be more skeptical. This is a good thing. The world needs strong and reliable crypto exchanges.

But do you know what the world doesn’t need?

Crypto banks.

Two days ago BlockFi, a centralized crypto bank that happens to share many investors with FTX, filed for bankruptcy. The failure rate for crypto banks is rapidly approaching 100%. BlockFi’s failure adds it to the scrap heap alongside Celsius and Voyager Digital. Nexo Bank is now the ‘last man standing’ in this niche. Nexo hails from the, shall we say, lightly regulated market of Bulgaria and still offers 12% rates on crypto deposits, without adequately explaining exactly how those yields are sustainable.

For some time now, I have believed that ‘crypto banks’ are an abomination – they are centralized institutions that do not adhere to crypto’s ‘first principle’ of decentralization, nor are they regulated like traditional banks. Decentralized finance (DeFi) platforms like Uniswap or Aave are not regulated, but they are generally safe and efficient because:

They are governed by open-source code that anyone can review. Thousands of armchair blockchain engineers compete to be the first to discover a vulnerability, which they either post on social media to warn others – or share it with the project team, who often pay a ‘bug bounty’ for the favor.

DeFi smart contracts are written and audited by some of the world’s best developers, who are paid higher rates per hour than partners at most top-tier law firms. This is as it should be, since these contracts routinely store hundreds of millions of dollars in locked value.

I’m not exaggerating about the energetic nature of armchair blockchain detectives on social media. For example, the first crypto insider trading arrest was made earlier this year when the Department of Justice arrested an OpenSea employee who was front-running sales of NFT projects that he had the authority to post on that marketplace’s home page. Do you really think that a career DoJ employee sniffed this out? The case was broken wide open on Twitter when an anonymous, eagle-eyed private citizen spotted that employee’s on-chain activity and posted the evidence for all to see.

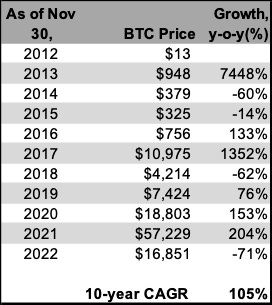

Bitcoin, and digital assets more broadly, are a revolutionary technology that also happen to be structured as financial instruments. Market pundits love to point out how Bitcoin has lost 70% of its value year-to-date. What they are ignoring is that Bitcoin has, on average, more than doubled in value every year for the past decade.

In November 2012, Bitcoin was trading on a handful of exchanges and peer-to-peer marketplaces for $13. Ten years later those same assets are selling on a highly liquid global market for $16,000. It is an unfortunate fact of life that, when an asset class appreciates over 1,000x in ten years, it is going to attract a swarm of scammers and bad actors. Obi-Wan Kenobi said it best…

‘Web 3.0’ has become a popular catchphrase for the vision of a new and improved Internet – one that transfers power from centralized platforms back to a platform’s users. Digital assets like Bitcoin and Ethereum will be the ‘payment rails’ of Web3, and will accrue value as billions of people use crypto to spend and send money online ‘peer to peer’, instead of through outdated banks and payment processors.

This progressive decentralization of online commerce will unlock trillions of dollars in value that, until now, has accrued to banks. It will also, for the most part, be immune to human corruption since decentralized applications are governed by code and not opaque management with hidden motives.

Centralized financial (CeFi) institutions like BlockFi were created to act as some sort of strange hybrid between a traditional bank and a decentralized lending platform – neither a bank, nor an application that is governed by code. The problem is that these banks have not been run transparently. Risk management teams were out to lunch while their trading desks opened enormous credit lines with shady institutions like Three Arrows Capital and Alameda Research. The latter defaulted on $680 million in loans, which was enough for BlockFi to be carried out on a slab.

Decentralized lending platforms like TrueFi and Maple Finance are completely transparent – anyone can check the custody wallet or smart contract to see how much capital is being lent out, and in many cases to whom it is being lent. One could argue that the level of transparency might be TOO high for many market participants, but the fundamentals at play here - namely, transparency and community-led governance - ensure that the platform operates with incentives that align with its users, not just those of its management.

CeFi businesses that we need

This is not to say that ALL CeFi institutions are bad actors or doomed to fail. Here are some examples of businesses that the digital asset market will still need going forward:

Exchanges

The market needs fiat on- and off-ramps, and crypto exchanges need to be widely accessible for this purpose. Coinbase and Gemini, both of which are domiciled in New York, serve this purpose well. Though New York continues to shoot itself in the foot with over-regulation (like its oppressive ‘BitLicense’) it nonetheless speaks well of a company’s bona fides when they are willing to endure the state’s burdensome requirements. Exchanges should be market-makers though, and that function should be shielded from any exposure to other, riskier, activities.

Custody Providers

There is a popular mantra in crypto: “not your keys, not your coins”. In other words, if you relinquish control of your digital asset wallet to another party then you have effectively relinquished ownership. Caveat emptor, etc. Veteran crypto investors know that a hardware wallet like Ledger or Trezor are the safest self-custody options for individuals. For institutions like hedge funds, many of whom are required to store their assets in custody with a third party, highly regulated companies like Anchorage Digital and Fidelity are available options.

Asset Managers

The vast majority of crypto companies and projects are still early-stage, and those companies need access to capital in order to grow. Decentralized autonomous organizations (DAOs) like BitDAO will likely one day displace traditional venture capital, but this is at best a decade-long trend that is still in its earliest days.

‘TradFi’ banks for crypto companies

Most traditional financial institutions (‘TradFi’ banks) are reluctant to offer services to crypto companies. Silvergate (NASDAQ: SI) and Cross River Bank are exceptions. Silvergate operates an internal network that allows for 24/7 instantaneous transfer of dollars or euros between its banking clients, which enables rapid movement of funds between crypto investors and other financial institutions.

*************

All of these business models are firmly rooted in the traditional financial services industry, and are required to help market participants transfer funds between fiat and crypto. The emerging ecosystem of ‘Web3-enabled’ businesses include DAOs, decentralized exchanges and P2P lending marketplaces and should have no direct link to the fiat-based financial system. Crypto banks like BlockFi failed because they tried to compete in both markets simultaneously, and ultimately failed to succeed in either one.